The US has a nonfiction crisis

The US has a nonfiction crisis

It's not just a Canadian thing

This is the 256th edition of SHuSH, the official newsletter of The Sutherland House Inc. If you’re new to SHuSH, push the button:

Sutherland House accepts submissions of manuscripts or proposals for nonfiction books (no agent required): submissions@sutherlandhousebooks.com

According to New York, we’ve just lived through the “summer of smut,” which the magazine celebrated with “a stimulating guide to the horny books all over best-seller lists and our TikTok feeds,” an Emily Gould meditation on the monster sex genre (“it’s not just about the extra-long tongues),” a piece on a romance-only bookstore, another on how to write great sex scenes, another how to make them sound even hotter in the audiobook—ten articles in all. If the bestseller lists are any indication, New York was onto something.

These are heady days for fiction generally. Nonfiction, not so much. I jumped from New York’s smutapalooza to a discussion of the sorry state of researched and fact-based writing in the always reliable Hot Sheet by Jane Friedman. Jane convened a panel of mostly writers and agents who, it turned out, were in general agreement with her thesis that “the model for producing researched nonfiction seems sidelined because big book deals now go to public figures, celebrities, online personalities.”

I was almost relieved to read this because I’ve tended to think that the decline of researched nonfiction is peculiar to Canada. It’s been one of the most consistent themes in SHuSH over the last five years. I still think it’s exacerbated here (and the Canada Council and federal cultural policy have a lot to answer for), but many of the problems we’re dealing with are also prevalent in the US, especially the economic ones.

Jane’s panel noted an across-the-board decline in the resources available to serious nonfiction writers. Fewer academics have the job security and sabbaticals and research assistants to take on major works. Fewer magazines and newspapers can sustain journalists on major reporting or research projects that might grow up into books. Those secure positions at news outlets that might hold a journalist’s job while they’re on book leave are disappearing. The big publishers who once paid advances that could sustain an author for a year or two while rooting through an archive or traveling around to interview people are instead directing ever larger sums to those celebrity projects, which are viewed as safer bets. Smaller publishers can’t afford to pick up the slack.

Said panelist Ann Kjellberg, author of the Book Post Substack and a former staffer at New York Review of Books, “for a lot of people, as a practical matter, they can only get a book deal if they can support a year of their life without working.” An established journalist at a major news outlet might still be able to get a six-figure advance to do some heavy lifting, she added, but “I have also spoken to editors who used to work for Big Five publishers… where all these titles that used to be written by historians and by journalists, where they’d be getting six-figure advances—they are just kind of dropping off the map.”

An agent, Carly Watters, concurred: “We know that nonfiction has been on a bit of a decline, and that makes it very hard for us to do our jobs in terms of the nonfiction projects that we want to pursue. I think the hard thing from my perspective is how do I approach somebody and say, ‘Hey, I think I can maybe get you a book deal. You’re an expert on this topic; I want you to take this much time out of your professional life to work on this book project,’ when they could turn that concept into a course and make money kind of immediately. Or monetize a Substack on that topic… and be well-known in that category.”

That’s another dimension of the problem. Some proportion of people who a decade or two ago might have written a substantial book are now instead dabbling in podcasts, newsletters, or YouTube channels. Some of them find the work as satisfying as writing—the feedback is instantaneous—although it’s equally unremunerative. The new platforms are as susceptible to blockbuster economics as the publishing world. They, too, lack a middle class. Nevertheless, says Watters, they might work for some talent. A prospective author might think, “‘Why do I need a book deal? If I’m monetizing this concept… as an expert, why does it have to be a book?’…. as somebody who’s advising authors, creatives, and experts on the best thing to do with their career, writing a book isn’t always the best thing for them right now.”

I tend to think the new mediums are inadequate substitutes for serious books and that momentum may shift back to the publishing world once the novelty wears off. It’s also true that various genres of literature are always moving in and out of style: today it’s smut; five years ago, at the height of the Trump presidency, there was a flood of political nonfiction. What’s worrisome are the declines in the business models that have long sustained researched nonfiction. These are long-term trends that show no sign of slowing and, as we’ve seen in the newspaper and magazine worlds, new business models are difficult to conjure. They beg the question asked by panelist Kjellberg: “who will produce the researched work in the future that people can rely on and be fully informed?”

Books remain the most reliable form of information about the world around us. They are still how most people learn of their history, their institutions of government, social affairs, science, technology, business, and the lives of significant people. Most of the podcasts and newsletters that treat these themes are dependent for their content on books.

In a time of misinformation and disinformation, competing versions of reality, echo chambers and filter bubbles, clickbait and sensationalism, declining trust in traditional media, to name just a few of the many diseases of our public sphere, well-researched and carefully constructed books based on verifiable fact are more necessary than ever, and more difficult to find.

We don’t hate our banks enough

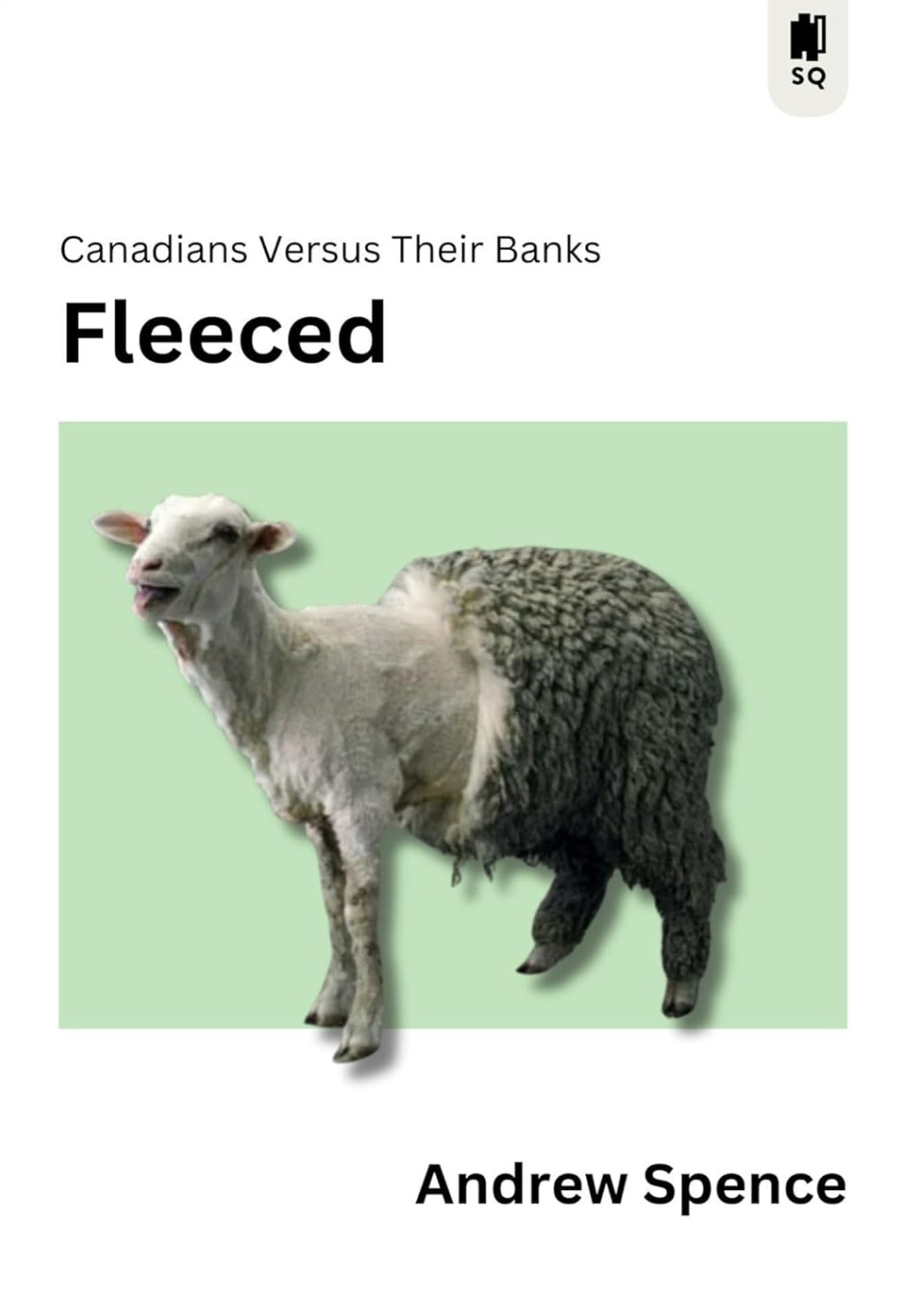

I could write about eight versions of this post based on the many revelations in Andrew Spence’s Fleeced: Canadians Versus Their Banks, the latest edition of Sutherland Quarterly, released this week. I’m going to run with the version most relevant to my fellow publishers and small business people in Canada.

Andrew lays out in aggravating detail how Canadian banks, although chartered by the federal government to facilitate economic activity in the broader economy, do all they can to avoid lending to small and medium businesses, never mind that small and medium businesses employ two-thirds of our private-sector labour force and account for half of Canada’s gross domestic product.

By OECD standards, small businesses in Canada are starved of bank credit, and when they are able to secure a loan, they pay through the nose. The spread between interest rates on loans to small businesses and large businesses in Canada is a whopping 2.48 percent, compared to .42 percent in the US—more than five times higher.

Why? Because Canada’s banks are a tight little oligopoly, impervious to meaningful competition. Their cozy situation allows them to be exceedingly greedy. Their profits and returns to shareholders are wildly beyond those of banks in the US and UK (and, as Andrew demonstrates, their returns from their Canadian operations are far in excess of those from the US market, meaning they screw the home market hardest.)

Our banks never miss an opportunity to impose a new fee, or off-load risk. From their perspective, small business involves too much risk—some of them will inevitably fail. The banks prefer that publishers and dry-cleaners and restaurateurs either finance themselves by pledging their homes, or use their credit cards to cover fluctuations in cash flow or make investments that will help them hire, expand, and grow. And that’s what entrepreneurs do. According to a survey by the Canadian Federation of Independent Business, only one in five respondents accessed a bank loan or line of credit. Half of respondents financed themselves, tapped existing equity and personal lines of credit, and about 30 percent used their high-interest credit cards.

(The banks, incidentally, claim they need to keep credit card rates around 20 percent because their clients are high credit risks when their own data shows the risk is minimal. They simply prefer to gouge customers. To a banker, forcing hundreds of thousands of small businesses to use their credit cards to finance their businesses rather than giving them proper small business loans at reasonable rates is great business.)

By severely rationing credit and making it exceedingly expensive, Canada’s banks siphon off an ungodly share of entrepreneurial profit to themselves while leaving the entrepreneur with all the risk. Their insistence on putting their own profits above service to the Canadian economy is one of the main reasons Canada has such a slow-growing, unproductive economy and a stagnant standard of living.

There is much else in this slim volume to make your blood boil: exorbitant fees on chequing and savings accounts; mutual fund expenses that torpedo investments; ridiculous mortgage restrictions, infuriating customer service…

On the latter point, I learned this summer that my local bank branch no longer has tellers. More astonishingly, it no longer has cash—if you want to withdraw funds, you are directed to a machine. The machines, of course, have caps on how much cash they dispense and charge fees per transaction. If you need more than the low daily withdrawal limit at the machines, you have to visit a branch downtown. The remaining employees in my branch are there to sell me things, not to provide service.

Fleeced: Canadians Versus Their Banks is a stunning exposé of the inner workings of our six major banks—something only a reformed banker and financial services veteran such as Andrew could write. He also explodes the myth that a bloated, uncompetitive banking sector is the price we have to pay for stability in times of financial crisis.

We are in desperate need of banking reform in Canada. Read this book and you’ll be shouting at your member of Parliament for prompt action.

Sutherland Quarterly is an exciting new series of captivating essays on current affairs by some of Canada’s finest writers, published individually as books and also available by annual subscription.

Subscribe to the Sutherland Quarterly Print subscription now, and receive a copy of the bestselling Justin Trudeau on the Ropes by Paul Wells.

Our regular reminder to readers to support independent booksellers. Click this link to make the above map come alive.

Our Newsletter Roll (suggestions welcome)

IF YOU’D LIKE TO BE INCLUDED, LEAVE A COMMENT BELOW.

Banuta Rubess’s Funny, You Don’t Look Bookish, reviews five books a week.

The Literary Review of Canada’s Bookwork, “your weekly dose of exclusive reviews, book excerpts, and more.”

Art Kavanagh’s Talk about books: Book discussion and criticism.

Gayla Gray’s SoNovelicious: Books, reading, writing, and bookstores.

Esoterica Magazine: Literature and popular culture.

Benjamin Errett’s Get Wit Quick, literature and other fun stuff

Lydia Perovic’s Long Play: literature and music.

Tim Carmody’s Amazon Chronicles: an eye on the monster.

Jason Logan’s Urban Color Report: adventures in ink (sign-up at bottom of page)

Anne Trubek’s Notes from a Small Press: like SHuSH, but different

Art Canada Institute: a reliable source of Canadian arts info/opinion

Kate McKean’s Agents & Books: an interesting angle on the literary world

Rebecca Eckler’s Re:Book: unpretentious recommendations

Anna Sproul Latimer’s How to Glow in the Dark: interesting advice

John Biggs Great Reads: strong recommendations

Steven Beattie’s That Shakespearean Rag, a newsy blog about books and reading

Mark Dykeman’s How About This: Atlantic Canadian interviews and thoughts on writing and creativity.

J. W. Ellenhall’s 3-Page Book Battles: Readers help her choose which of three random books to review each month.

Donald Brackett’s Embodied Meanings: “Arts music films literature and popular culture.”

THANKS FOR READING. PLEASE SHARE, OR LEAVE A COMMENT, OR SIGN UP, OR CONVINCE SOMEONE ELSE TO SIGN UP:

Thanks for this. Your advocacy and your willingness to put your money where your mouth is helps keep hope alive (to coin a phrase).